When I graduated from high school in 1989, I was so excited to start pharmacy school at Duquesne University in Pittsburgh, PA. My parents were very happy for me but told me that it would be very expensive and that I was going to have to take out student loans. I thought I understood since I knew it was something that they could not afford. I was well aware that I was going to be responsible for paying back the loans back however, I did not think much about it until that 6-month grace period was up and the bills started coming in. Although I did receive a few scholarships and the Pell Grant, the price tag for my Bachelor of Science in Pharmacy degree in 1994 was over $60,000. I had Stafford loans, Parent Plus loans and a private loan. That may seem low compared to today’s average cost of $170,000 but the salary was about $50,000 compared to today’s average of $120,000.

When I graduated in 1994, I was 23 years old and in charge of all of my finances for the first time in my life. At first, I really didn’t know what I was doing and made a lot of mistakes. I leased my first car, did not have an emergency fund and started to build up credit card debt. At that time, there weren’t many people talking about or teaching personal finance. It was also embarrassing to tell other people that you were in debt.

WAKE-UP CALL

In 1998 I was driving to work and started listening to the Dave Ramsey show on the radio. He had a segment where people would call in and scream that they were debt free. It really started me thinking about when I would be debt free. When I got home, I started adding up all of my debts and came to the conclusion that I was BROKE! Not only did I still have student loans, but now I also had a house payment and $10,000 in credit card debt. I would not even own my car after my lease was finished. I had a net worth that was negative $150,000. Yes. I said negative. I would look at that list of debts and it would keep me up at night. It was very stressful and scary. I wondered how in the world I was going to pay off everything and if I would ever get rid of this burden. The crazy thing is that my house was not extravagant, and neither was my car. I was just like every other young pharmacist that I knew. I was earning a high salary, but the money was gone before it even came in.

FROM BROKE TO DEBT FREE

In January 2010 I became completely debt free (including the mortgage) for the first time in my life. The key was changing my mindset and behavior with money. I began by decreasing my spending and paying off that credit card debt using the debt snowball method. I then took that extra money (and any raises and bonuses) and started making double and then triple payments on my student loans. I made my final student loan payment in June 2001. I was able to pay them off in 6 and a half years which I felt really good about. I purchased my first car without a lease in 2002. I took the extra money that I had from having no more student loans and paid that loan off in 2006. Then I took all that extra money and applied it to my principal house payment. I took my final payment to the bank and paid my house in full in January 2010. All the while I was able to save up an emergency fund as well. I felt truly free of that burden of debt, and it was such a relief.

DEBT FREE THE SECOND TIME

In 2016 my husband and I got married and bought a new house, so we were back in debt for a little while. I was able to take the money from selling my first house, so we only had to mortgage $235,000. Applying the same debt snowball that I used before, we were able to pay off our new home in three and a half years. It was February 2020 just as the pandemic was starting. I was also able to replace my 10-year-old car and pay cash for it. Becoming debt free has allowed me to leave my full-time retail position in 2020 at the age of 49 to work part-time. It has also allowed me to begin my passion as a financial coach to help other pharmacists achieve financial independence as well.

FINANCIAL FREEDOM IS POSSIBLE

From 1994 to 2016 my salary steadily increased until it hit a plateau. From 2016 until I left retail in 2020 my salary actually started to go down and then stagnate. So, I understand what pharmacists are facing today. The high debt to income ratio can be frustrating and frankly, scary. It can be very stressful, but I want to give you some hope. Once I got serious about getting out of debt, I was able to pay off over $700,000 in 22 years. This included student loans, 3 car loans, 2 houses, and credit cards. If I could do it, I know you can do it.

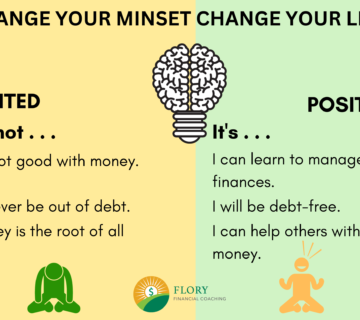

I believe that all pharmacists can and should be debt free and able to have a net worth of at least $1 million. When I talk with other pharmacists, I keep hearing the same stories. They make a six-figure salary, they are working full time, but they are still living paycheck to paycheck. I am here to tell you that you can get control of your finances, but it will take hard work, dedication and most importantly, a change in your mindset. You need to intentionally plan where your money is going instead letting your money control you. David and I have been able to spend our money on things that align with our values.

Tracking your expenses, budgeting and having an emergency fund are the first steps to attaining financial freedom. Once you can get that under control, then you can start investing and building an income that is passive. That is how my husband and I have been able to increase our net worth to over $1 million! This will give you the ability to work in pharmacist roles that will lead to a happy life instead of staying in a job for fear of losing that paycheck or benefits they offer. The sooner you start your plan, the sooner you will reach your dreams!

{kind=link}